Apparently, banking executives’ DNA, customer relationships legacy, and even banking infrastructure adjusted to the most traditional business models appear to contribute to a sense of complacency as far as finding new customers and keeping the existing ones. Back in 1994, Bill Gates said that although banking is necessary, banks are not. Banks continue to exist, however many of their financial services are undergoing striking transformations.

Banks are learning from social networks and major fintechs, where customer preferences, in-depth demographic studies, and big-data analytics form the backbone of the predictive sales model. Let me illustrate it with a real-life story based on my recent online shopping experience.

I recently searched for a wrist watch as a birthday present for my teen-age son. After an hour of web research, I got bogged down with unlimited choice and sales pitch type of narratives instead of the precise information I needed. It happily ended the same evening as I was skipping through the news-line with a social network app on my mobile casually suggesting the right kind of watch ad with some easily accessible information on functions to go with it. The choice and decision were easy. Then I made a phone call and arranged a delivery.

I am one of those people who dislikes going to shops and bank branches largely thanks to sales staff invariably offering me things and products I don’t need in a way that makes me uncomfortable to say no.

It is for this kind of people (and you’d be surprised how many of us there are) as well as for their teenage children that ‘shoppable’ content will be filling in an important gap, where a convincing story on social media gets transformed by a few clicks into a smooth customer journey and effortless secure payment with e.g. Apple Pay. Recent studies by MacEwan University and Microsoft explain why it is critical: due to multi-tasking, smartphone use and content inundation, consumers can now only focus for 8 seconds, while goldfish have a 9-second attention span.

It is quite hard to imagine, but even good old online banking is on its way to becoming obsolete. According to Mark Ryan, Chief Analytics Officer at Extractable, “in the next 5 to 10 years, we will most likely see web traffic to banking sites and mobile applications drop by over 50%. We know that an average of over 50% of the traffic to online banking through browsers and mobile applications is there to perform the simple task of checking a balance and then leaving”.

One of Gartner’s predictions is that by 2020, 30 percent of web browsing sessions will be done without a screen thanks to new platforms based on "voice-first" interactions

Furthermore, intelligent personal assistants and smarter chatbots are already offering a missing link in terms of interaction, feedback, support and well-informed advice.

In banking, these technologies help transform resource-intensive and full-time staff dependent processes and operations into semi- or fully automated interactive communication experiences. Communicating with a ‘talkbot’ can be emotional in a way, but it is a safe space as far as preventing the very possibility of inter-personal tensions or embarrassment, as it is a human-machine dialogue after all.

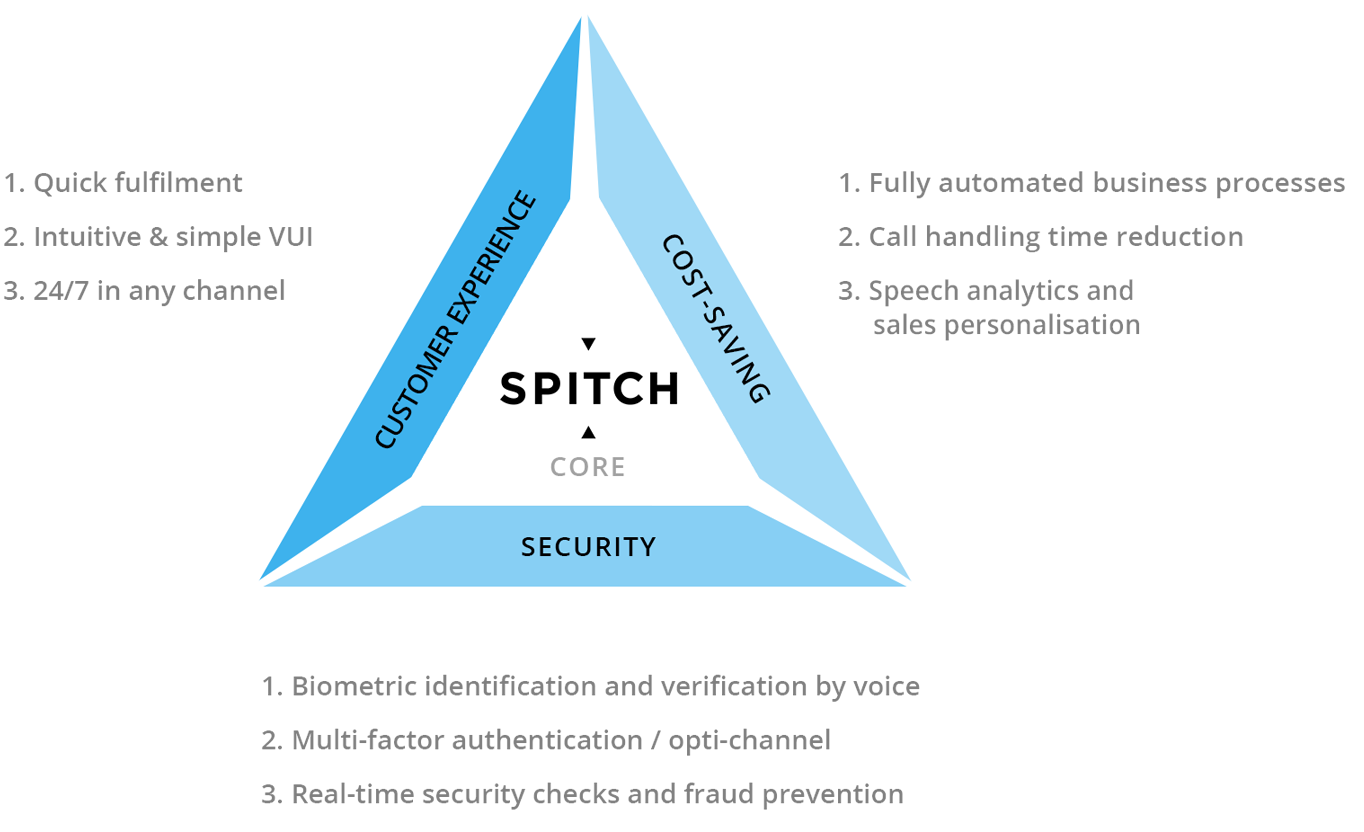

The emotional side of communication comes with hearing a natural and attractive human voice from the machine. Business process re-design enabled by the progress in natural language processing (NLP) and voice biometrics technologies is particularly important for customers who still prefer to fix an issue by preferably just one, short, and pleasant phone call.

To deliver the best performance in a business sense, the entire spectrum of speech technologies from voice biometrics to sentiment analysis and semantic interpretation should be deployed as a well-tailored combination meeting a concrete set of needs. This works best for wealth management, standard enquiries and insurance claims processing, banking guarantees quotes in some markets etc.

Research labs in certain larger banks are now busy studying how investment robo-advisers with a voice user interface and multifactor authentication with a voice biometrics capability could transform clients’ dynamic portfolio management, for example. But there is more to it than pure business efficiency and customer satisfaction. It’s about factoring in social value based on unstructured data.

To cut a long story short, I would rather try to outline the contours of a new era of responsible ‘talk banking’. Responsible in a sense of being:

Bringing artificial intelligence with a VUI layer into the picture would add a few more items on the above list. Paradoxically, VUI makes artificial intelligence less artificial and more ‘intellectual’ for a human perception. Most importantly for banks, new client onboarding, discreetly conducted fraud prevention, and KYC requirement fulfilment will probably be the first to deliver responsible and less costly improvements in customer experience and effective sales due to reduced full-time staff exposure.